The Cost of Health Insurance in Massachusetts

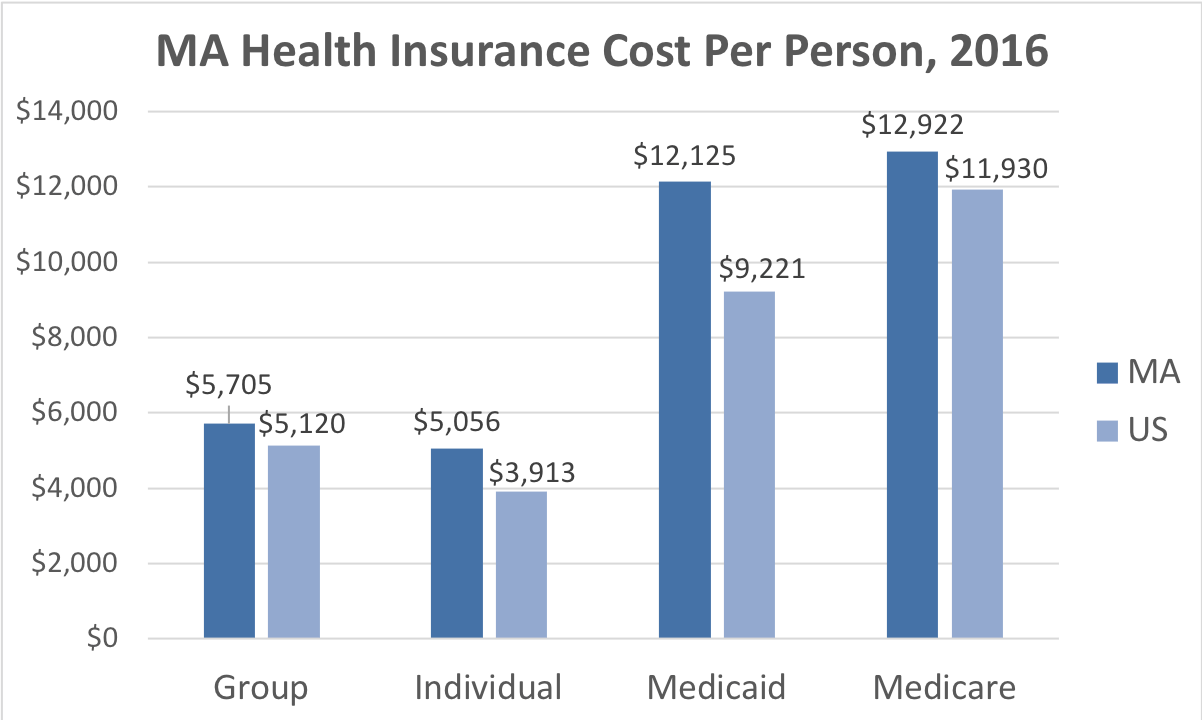

The average cost of health insurance in the state of Massachusetts is $8,068 per person based on the most recently published data. For a family of four, this translates to $32,272. This is $1,087 per person above the national average for health insurance coverage. However, health insurance costs vary significantly based on the cost of care and the population insured. The chart below shows the four major insurance types available in Massachusetts. The dollar amounts shown on the chart are the average cost in Massachusetts to insure people for each type of insurance.

Massachusetts Health Insurance Cost Per Person

Average cost calculations for comprehensive group and individual insurance is based on data reported to the state department of insurance. Group insurance is based on 1,538,926 enrollees and Individual insurance is based on 341,803 enrollees. Supplementary vision and dental insurance contracts sold as riders to comprehensive insurance are not included. Medicaid costs are based on data from Macpac.gov divided by the number of people covered based on Kaiser Family Foundation data. Medicaid data includes both state and federal spending. Medicare costs are based on data from CMS.gov divided by the number of people covered based on Kaiser Family Foundation data. CMS data are from 2014, adjusted for health insurance cost inflation rates.

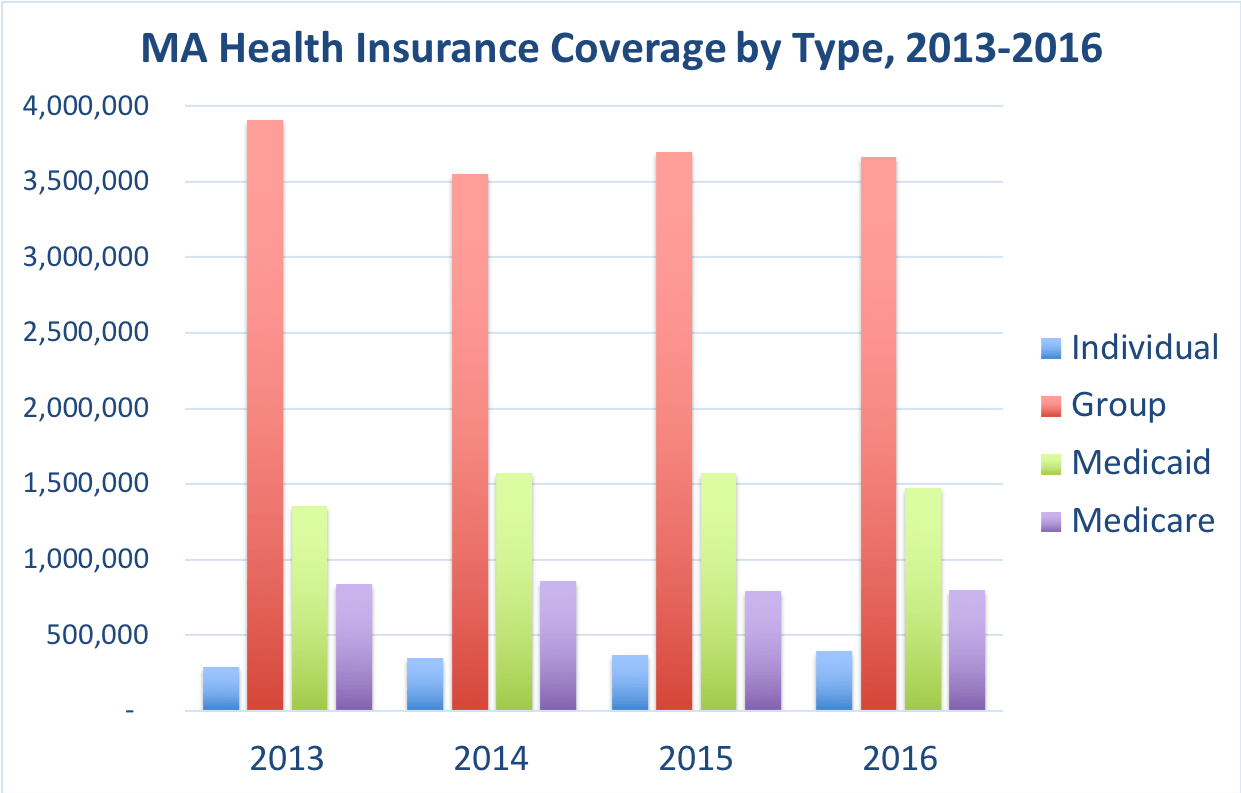

Number of People Covered by Health Insurance in MA

The chart below shows the number of people insured wth each type of insurance plan available. The most recent reported year plus three years of history is shown.

Number of People Covered by Type of Health Insurance

Data from the Kaiser Family Foundation.

Trends identified in the above data include an increase in the number of people with individual and Medicaid coverage. The number of people insured with group coverage in Massachusetts shows a slight decline while the number of Medicare enrollees is relatively flat.

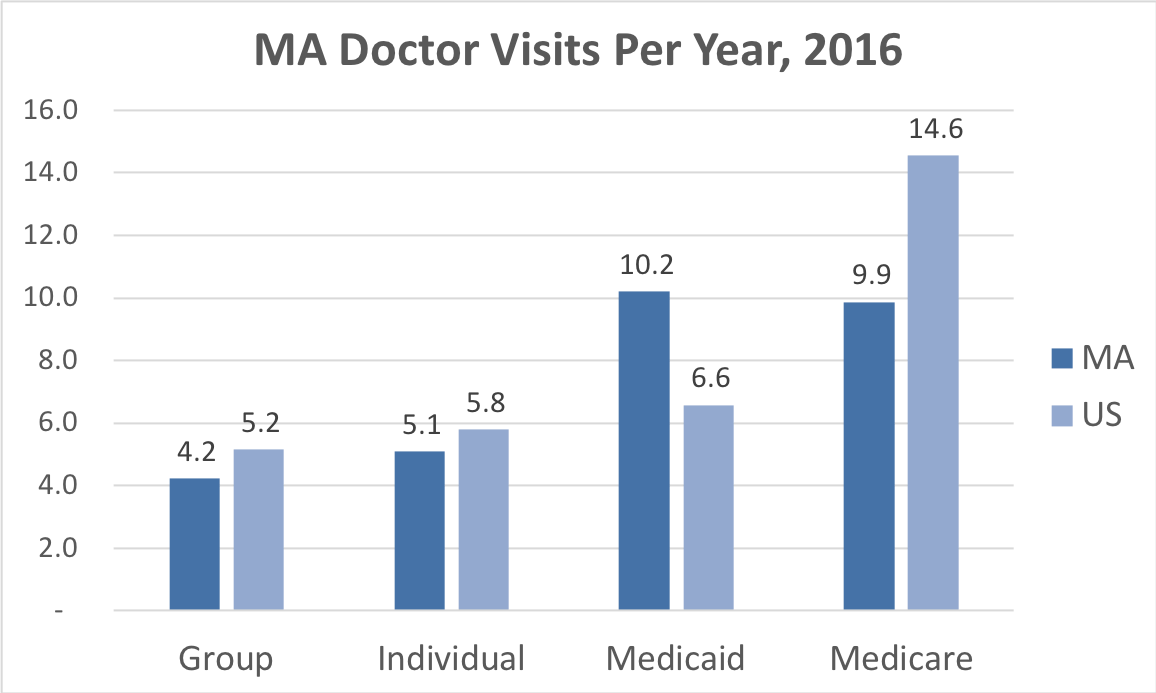

Health Services Use by Massachusetts Residents

The tables below show the frequency with which residents use health services. The data are collected from insurance company filings with the state insurance department. The number of enrollees on which data was collected is as follows: Group insurance, 1,538,926; Individual insurance, 341,803; Medicaid managed care, 843,489; and Medicare Advantage, 187,005.

MA Doctor Visits, Per Person, Per Year by Insurance Type

This type of care includes visits to doctors in which the patient was not in an institution such as a hospital.

The frequency of doctor visits among all user categories are reasonably close to the national average, with the exception of Medicaid managed care patients. Medicaid managed care patients run about two-thirds higher than the national average, other patient types are about 10% below the national average. Other than Medicaid, we don't see the frequency of doctor visits among Massachusetts residents as a contributor to the high health care and health insurance costs.

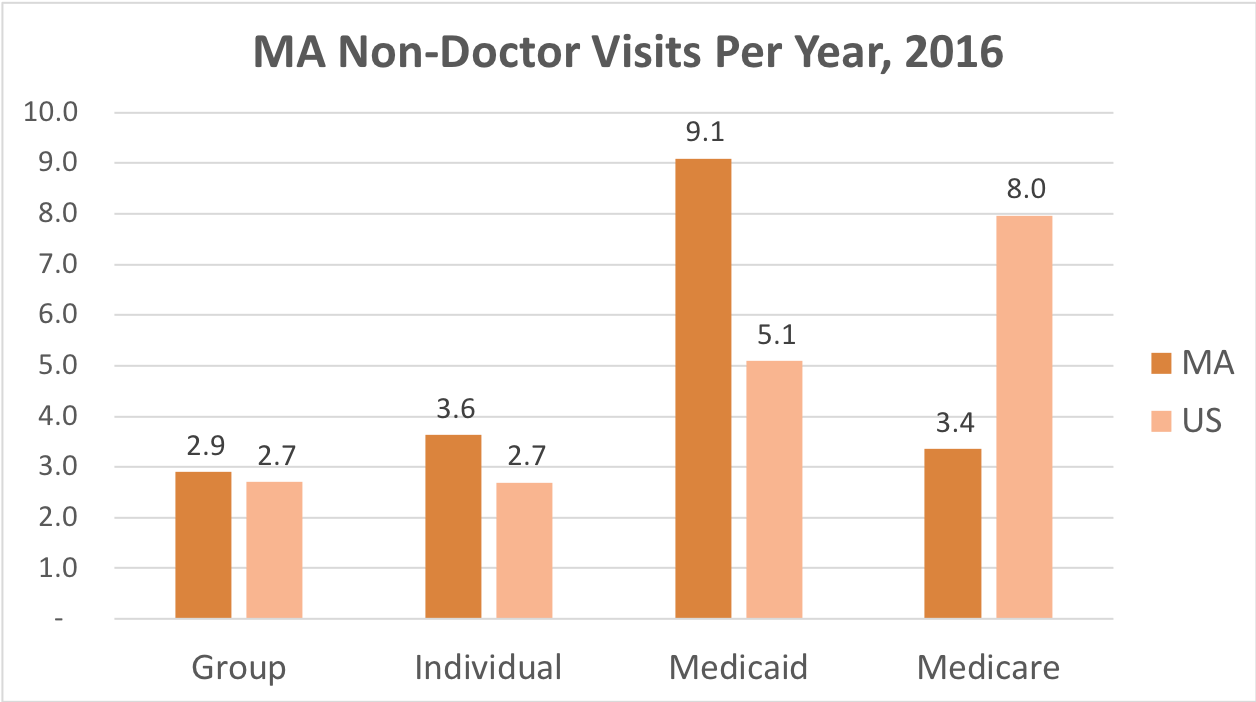

Frequency of Using Medical Services Other Than a Doctor or Hospital

Non-doctor health care visits is a measure of how often people receive medical care without seeing a doctor. This type of care excludes patients that have been admitted to hospitals or other institutions. Examples of non-physician health care includes appointments or walk-in clinics to see a nurse, physical therapist, counselor for mental health appointments or other non-physician medical personnel.

Both Medicaid managed care and individually insured patients have a high rate of use for non-physician care in Massachusetts. Medicaid managed care patients in particular is very high at nearly double the rate of the national average. Non-physician care tends to be an expensive form of treatment.

The reason non-physician visits are expensive is that many times these are visits to outpatient facilities. Most outpatient facilities are owned and operated by hospitals. While hospital owned and operated medical facilities are less expensive than a hospital, oftentimes they are more expensive than a doctor visit.

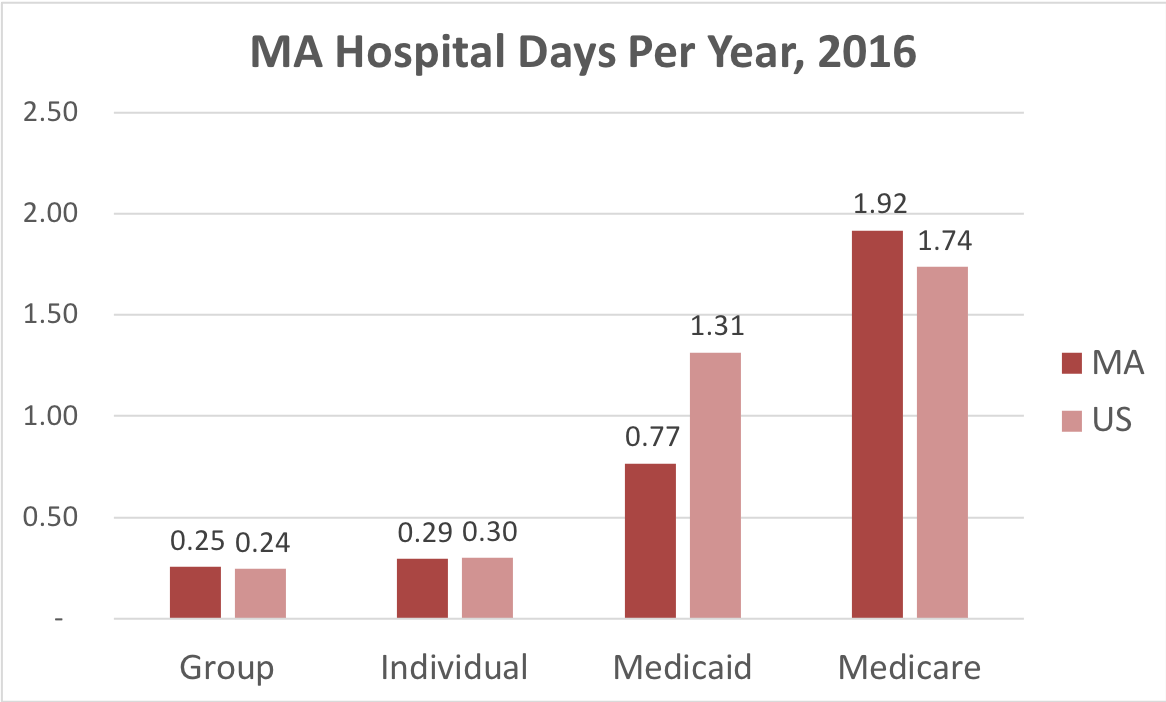

Average Number of Days MA Residents Spent in the Hospital

The number of days in the hospital are counted starting with the day the patient is admitted. The last day is not counted, unless the first and last day are the same day.

Massachusetts residents covered by group and individual insurance plans spent an average number of days in the hospital. Medicaid managed care patients spent a below average number of days in the hospital while Medicare Advantage patients spent more days than average in the hospital.

Health care Market Competitive Dynamics

Most states have laws requiring new health care facilities to be approved by special boards. These boards are known as "certificate of need" (CON) boards. The purpose of these boards is to certify there is need for new facilities. CON boards have the effect of reducing the level of competition, which results in higher prices for the services provided.

To quantify the effect of legislation that minimizes competition, ValChoice has calculated the difference in health care cost between states with and without CON boards. Using a simple average calculation, states with CON requirements have an average cost for health care that is $655 more per person insured than states without CON requirements.

States included in the calculations as having CON requirements include the following: Alabama, Alaska, Arizona (modified CON), Arkansas, Connecticut, Delaware, District of Columbia, Florida, Georgia, Hawaii, Illinois, Iowa, Kentucky, Louisiana, Maine, Maryland, Michigan, Minnesota (modified CON), Mississippi, Missouri, Montana, Nebraska, Nevada, New Jersey, New York, North Carolina, Oklahoma, Ohio, Oregon, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, Washington, West Virginia, Wisconsin (modified CON). Other states do not have CON board certification requirements.

The Effect of Insurance Deductibles on The Cost of Health care

MA residents insured through group, individual and medicare health plans generally have a deductible. Deductibles define the amount of the medical expenses the insured person must pay before the insurers coverage begins to pay the medical bills. The deductible amount depends on the insurance plan. Generally speaking, individual insurance has larger deductibles than other plans. Deductibles have the effect of increasing the cost of the insurance for people that file insurance claims. For example, a person on an individual plan paying the average price of $5,056 with a relatively common $6,000 deductible has an effective price of more than $11,000, if they use their insurance.

Overview of The Different Types of Health Insurance Plans

Individual Coverage

The individual health plan is for people who do not qualify for other types of insurance. This type of insurance is often referred to as Obamacare or the Affordable Care Act (ACA). Self-employed and unemployed people who are not eligible for employer provided insurance often purchase individual coverage. The premiums earned under this type of insurance are based on the premiums paid by the individual. Tax credits provided to make the insurance affordable are not included in the premiums earned. Individual coverage includes all types of plans. The basic plan types are referred to as Bronze, Silver and Gold Plans.

Group Coverage, Also Known as Employer-Sponsored Health Insurance

Companies that provide health insurance to employees as a benefit provide an insurance type known as group insurance. The cost of this type of health plan is based on total premiums paid to the insurance company. Premiums include payments from both employers and employees. Premiums do not include payments for services such as deductibles, co-pays or other out-of-pocket costs. Group coverage includes: Health Maintenance Organizations (HMO), Preferred Provider Organizations (PPO), Point-of-Service (POS) Plans and High-Deductible Health Plans.

Medicaid and CHIP

Medicaid total cost and enrollment numbers include the Children’s Health Insurance Program (CHIP). These programs provide health insurance coverage that is not included under Medicare coverage. Examples of the type of health coverage provided includes doctor visits, hospital expenses, nursing home care and home health care. Medicaid also covers long-term care costs, both in a nursing home and at-home care. The costs associated with medicaid is inclusive of both state and federal spending.

The data on how Medicaid patients use health services is based on Medicaid managed care. Medicaid managed care provides for the delivery of Medicaid health benefits and additional services through contracted arrangements between state Medicaid agencies and managed care organizations (MCOs) that accept a set per member per month (capitation) payment for these services. The capitation model is unique in that it is not a pay for service. Instead, this is a set fee paid per member, per month, whether or not the person seeks service.

Medicare and Medicare Advantage

The charts showing the cost the the number of enrollees includes people covered by all types of Medicare and Medicare Advantage. The cost of this type of health coverage includes participation from employers, individuals, federal, state and local government. Excluded from the costs are any form of co-pay or a deductible the individual must pay to receive care.

How enrollees use their health care services is based on enrollees in Medicare Advantage plans only. Medicare Advantage plans are Medicare health plans offered by private companies that contract with Medicare. Medicare Advantage plans include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Private Fee for Service Plans, Special Needs Plans and Medicare Medical Savings Account Plans (MMSAPs).