Hurricanes are on the mind of much of the U.S. right now. Hurricane Henri hit the NE last week. This week Ida battered Lousiana, then continued north with torrential rains. Homeowners from Florida to Maine are now wondering if they need hurricane insurance. Knowing that insurance can be confusing, ValChoice set out to make hurricane insurance easy to understand.

The confusion is often due to how deductibles are handled. In many states, the deductible for wind damage related claims increases when there has been a hurricane.

Start your insurance journey by understanding how good your current auto and home insurance are. Just click the buttons below to find out.

What is hurricane insurance?

Historically, homeowners policy deductibles applied to hurricanes and windstorms. However, the severe damage of catastrophic storms like Hurricane Katrina necessitated insurance companies minimize losses from these events. An easy way to minimize losses is through larger deductibles. Therefore, insurance companies instituted a new way of calculating deductibles when damage is caused by wind.

Hurricane insurance isn't necessarily a different type of insurance. Depending on where you live and who your homeowners insurance company is, hurricane insurance can be part of your homeowners policy. The difference from the the traditional homeowners policy is that the deductible may be larger. Also, the deductible is calculated differently. Importantly, the increase in the deductible amount is often significant.

Do I need hurricane insurance?

Homeowners insurance policies typically have a dollar deductible. $500 and $1,000 are a common deductible amounts. No matter how much damage you have with a dollar deductible, you pay the amount of the deductible.

However, hurricane deductibles are based on a percentage of the insured value of the home. For example, if the insured value of your home is $500,000, here's what you would owe. With a 2% deductible you would pay the first $10,000. With a 5% deductible, you pay the first $25,000. In this example, the difference the homeowner would owe could be as much as $24,500.

The percentage options that are available for deductibles are determined by state law. This means the regulators in your state define the options. Insurance companies can then offer from the options approved by the state regulators. Therefore, most insurance companies will offer similar options.

Which states have hurricane deductibles?

If you live in one of these 19 coastal states, or Washington D.C., you may have a percentage deductible for your hurricane insurance. Alabama, Connecticut, Delaware, Florida, Georgia, Hawaii, Louisiana, Maine, Maryland, Massachusetts, Mississippi, New Jersey, New York, North Carolina, Pennsylvania, Rhode Island, South Carolina, Texas, Virginia and Washington DC.

To avoid confusion, you should also know that hurricane deductibles are often also referred to as a wind deductible. The good news is that hurricane insurance is not hard to get. In fact, you can buy a wind insurance policy from the same company from whom you buy homeowners insurance. The bad news is, if you need wind insurance you are likely to have to pay a higher price than if you didn't need wind coverage.

Hurricane Overview

Some background on hurricanes is helpful for understanding the deductible options you may have. This can also be helpful for understanding when your deductible may change from a typical dollar deductible to a percentage.

Hurricanes form over open water that is 26.5 degrees C (80 degrees F), or warmer. This fact explains why the most severe hurricanes hit the southern U.S. where the ocean temperatures are highest. Hence, hurricanes hit these coastal areas with the most energy. Once hurricanes move over colder water or land, they begin losing energy.

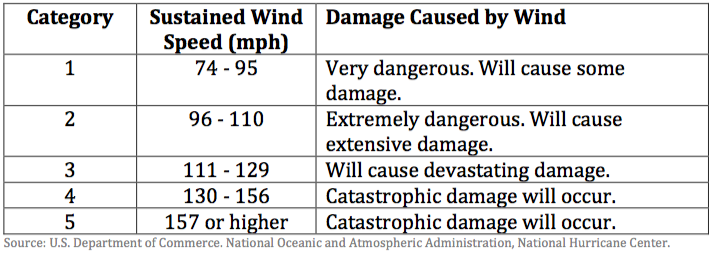

Hurricane severity is measured on a standardized scale. The scale is known as the Saffir-Simpson hurricane wind scale. The scale categorizes hurricane strength based on the average, sustained wind speed over a one-minute period. Below is a summary of the Saffir-Simpson wind scale.

When hurricane deductibles become effective varies by state. However, many states use the category one definition of the Saffir-Simpson scale as the minimum storm strength to trigger hurricane deductibles. This means the 74 mph minimum speed of a category one hurricane is a common qualifying event that changes your deductible from a dollar amount to a percentage.

Hurricane Deductibles vs. Windstorm Deductibles

While they are similar, there are important differences between hurricane deductibles and windstorm deductibles. Both are similar from the point-of-view that they change the deductible amount. However, they are different in terms of what they cover and how the deductible changes. The following is a brief summary of different types of insurance against wind damage.

The most broad application of increased deductible amounts is the windstorm deductible. Windstorm deductibles apply anytime damage is caused by wind. This includes tornadoes, thunderstorms, tropical storms, Nor 'easters and hurricanes. Windstorm deductibles are common in areas with a high frequency of tornadoes and thunderstorms.

A more costly deductible than the windstorm deductible discussed above is the "named storm" deductible. This type of deductible is less common than the windstorm deductible discussed above, and typically has lower deductible amounts than the hurricane deductible. Named storm deductibles apply when the storm causing the damage is identified by an official name.

The most costly form of deductible for consumers is the hurricane deductible. Hurricane deductibles commonly apply to coastal areas. The 19 states plus Washington D.C. listed above are the states where state law currently allows hurricane deductibles.

How to Choose the Best Homeowners Insurance Company

Deductibles are one of the considerations when choosing a homeowners insurance company. Another important factor to consider is how well the company performs when paying claims.

If windstorm deductibles are part of your consideration for homeowners insurance, you live in an area with a high risk of home damage from wind. That means your likelihood of filing a claim is higher than for most homeowners. In this situation you need to pay attention to the claims handling performance of insurance companies. Not considering this important factor could lead to large financial losses following a storm.

ValChoice makes finding the best insurance companies easy by listing the best companies in each state. Click on the list below to go directly to the best auto and home insurance companies in the 19 states with wind deductibles

Comments are closed.